The UAE and Saudi Arabia are witnessing a rapid shift toward digital payments, with digital wallets (Apple Pay) emerging as the fastest-growing payment method. According to the Worldpay Report 2024, in the UAE, digital wallet usage in online retail is set to rise to 42% in 2027, overtaking credit cards, while Point of sale (POS) transactions will see use of digital wallets rise from 22% to 35%. In Saudi Arabia, the growth in digital wallets is expected to rise from 24% to 36% for online retail and from 22% to 37% in POS transactions, fueled by MADA’s 93% market share in card payments.

Governments and regulators in the region are playing a key role in driving this growth. Saudi Arabia's Vision 2030 program aims to increase the share of cashless payments to 70% by 2025, demonstrating both the ambition and the capacity to drive this transformation. Similarly, the UAE has implemented the Smart Dubai initiative, which is focused on stimulating the digital payments ecosystem and encouraging the expansion of online retail.

In this article, we highlight the top trends shaping digital payments in MENA for 2025. We also provide tips to improve your payments strategy based on these trends to improve revenue, strengthen data security, and grow customer satisfaction.

1. Use of AI in Fraud Prevention: Strengthening Payment Security with Generative-AI models

- Based on the National News the average cost of a data breach in the Middle East rose 8.4% annually to $8.75 million in 2024.

Fraud prevention and digital payment security need a stronger, more proactive approach in 2025. The Merchant Risk Council highlights that using GenAI is key to staying ahead of evolving threats. Unlike traditional AI models, GenAI improves fraud detection with smarter rule-building, better accuracy, and real-time adaptability—helping businesses protect their assets more effectively.

Building on this approach, Amazon Payment Services developed an advanced fraud detection & prevention solution to ensure secure payment processing for Enterprise merchants in the high-risk category business. This tool has unlimited rule building capability with no dependency on 3P, faster processing times, and better uptime. The convergence of AI and machine learning with traditional systems allows companies to enhance fraud detection accuracy and prepare themselves against emerging fraud schemes, that are unfortunately becoming more effective with every attempt. The financial stakes are particularly high in industries like insurance, where fraud could result in substantial losses.

“As fraud schemes become more sophisticated and the financial stakes continue to rise, businesses must shift from reactive to proactive fraud detection strategies. It’s essential to implement systems that can adapt in real-time and identify emerging threats before they cause significant harm. In high-risk industries such as insurance, where the impact of fraud can be devastating, staying ahead of these threats is not just a best practice—it’s a business imperative.”

- Ibrahim Eladawi, Head of Financial Crimes Compliance and Risk, Amazon Payment Services

2. Predictive AI: Reducing Cart Abandonment and Optimizing Payments

- Market size projections indicate that the UAE’s online retail industry will grow at a 12% CAGR(Compound Annual Growth Rate), reaching $46B by 2027, while Saudi Arabia will see a 15% CAGR, hitting $32B based on the WorldPay Report 2024.

- POS transactions will also expand in 2027, with the UAE reaching $180B and Saudi Arabia reaching $236B.

Globally over 70% of potential online sales are abandoned by customers before completion. This represents a significant loss of revenue for retailers. Businesses can gain real insights into changing patterns of customer preferences using AI-driven customer analytics. These insights can be leveraged to enhance the online shopping journey at an individual level through hyper-personalized user experiences, personalized product recommendations, dynamic pricing, and improved customer service.

Leveraging AI in efficient ways, merchants can also optimize payment experiences by positioning and recommending tailored payment options for customers. For instance, when a customer is attempting to buy a high-value item like an iPhone, merchants can suggest BNPL solutions or Installments to make the purchase more affordable. Alternatively, they can encourage quick card payments by offering instant discounts. Amazon Payment Services enables merchants in the region to accept Credit Card Installments and BNPL seamlessly, providing a unique offering that empowers businesses to enhance customer affordability and drive conversions.

3. Real-Time Payments: Need for Speed and Efficiency on a Rise

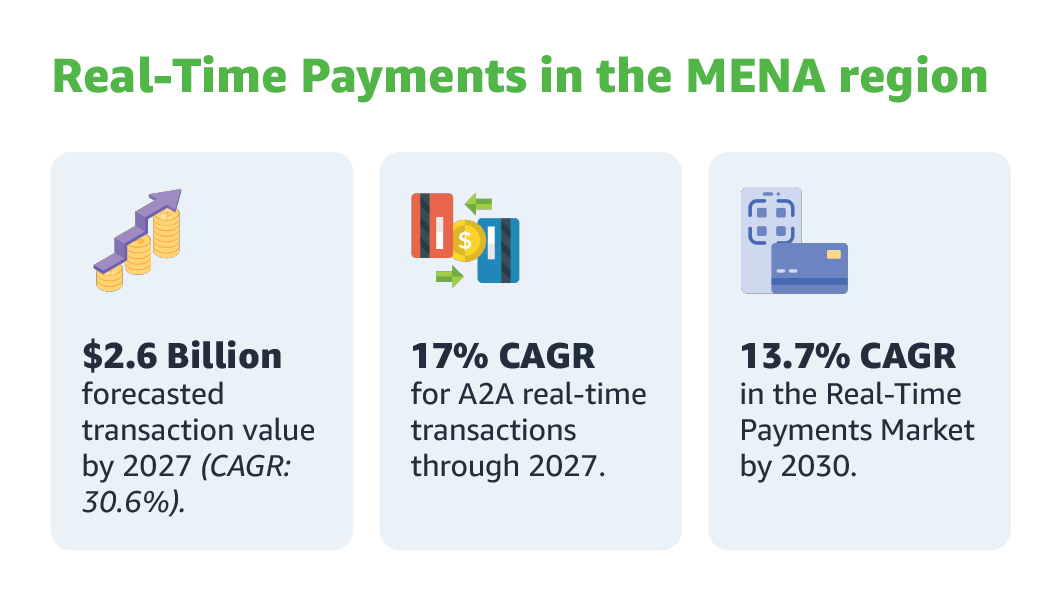

- According to ACI Worldwide, with transactions in the region expected to surge from to $2.6billion by 2027, representing a compound annual growth rate (CAGR) of 30.6 per cent.

- Account to account (A2A) real-time transaction values across the region are forecasted at 17% CAGR through 2027 as per the WorldPlay Global Payment report 2024.

- MENA’s Real Time Payments Market is expected to register a CAGR of 13.7% by 2030.

With the widespread adoption of real-time payments, customers now expect faster and more efficient payment options, leading to the growth of real-time payments in the region. This includes request-to-pay services, which businesses can leverage to optimize cash flow, reduce payment delays, and streamline payment processes. Saudi Arabia and the UAE are leading the charge in economic transformation with strategic initiatives like Saudi Vision 2030 and the UAE's National Digital Transformation Strategy to enhance financial markets and drive the adoption of digital payment systems. With consumers and businesses increasingly seeking more cost-effective, expedient, and efficient payment methods, and greater merchant acceptance of real-time payment solutions, consumer and commercial adoption is rapidly accelerating.

Globally, merchants and consumers are now embracing real-time payments through apps, QR codes and mobile wallets. The power of collaboration between governments, regulators, banks and FinTech is now resulting in wider domestic reach and new use cases.

4. Innovative Payment Solutions: Omnichannel Strategy to Enhance Consumer Convenience

Consumers today expect seamless payment experiences across multiple channels, from online retail websites to mobile apps and in-store transactions. Omnichannel payment strategies, which integrate various payment methods, are becoming essential for businesses aiming to provide a consistent and convenient checkout experience. Digital wallets, social commerce, and in-app transactions are key drivers of this trend, contributing to higher customer satisfaction and increased sales. Innovative payments like voice-enabled transactions, making payments using palm and frictionless retail shopping are changing the way businesses can accept payments.

Central banks across MENA, particularly in countries like Egypt, Bahrain, the United Arab Emirates, and Saudi Arabia, have implemented progressive policies. These policies aim to deregulate digital payment services and establish robust financial infrastructure. These regulatory changes have created a more conducive environment for financial institutions and technology providers to introduce innovative payment solutions.

5. Network Tokenization: Enhancing Security and Efficiency

- The tokenization market in the MENA region is projected to grow at a compound annual growth rate (CAGR) of 19.3% from 2024 to 2031.

Network tokenization in the MENA region is a payment security solution that replaces sensitive credit card details, with a unique, encrypted token issued by card networks like Visa or Mastercard. Instead of storing actual card information, this method enhances security by minimizing the risk of data breaches for both merchants and consumers.

By enabling secure online transactions, network tokenization also streamlines payments across various platforms and devices, delivering a safer and more seamless payment experience in MENA.

How Network Tokenization Works

- Card Information Entry: The customer provides their card details on a merchant’s website or mobile app, which are securely transmitted to the card network.

- Token Creation: The card network generates a unique token that replaces the actual card number, ensuring sensitive data remains protected.

- Payment Authorization: The merchant processes the transaction using the token instead of the original card details, sending it to the issuing bank for approval. This ensures the actual card number is never exposed during the transaction.

Conclusion

The digital payments space in MENA is transforming rapidly, driven by evolving consumer preferences, technological advancements, and regulatory changes. Businesses that embrace trends like AI-powered fraud prevention, predictive analytics, real-time payments, and omnichannel experiences can thrive. Governments across MENA are playing a key role in advancing the adoption of Central Bank Digital Currencies (CBDCs), which are expected to revolutionize the way consumers and businesses engage with money. The emergence of central bank digital currencies (CBDCs) further accelerates financial inclusion and modernization, offering a seamless blend of traditional and digital transactions. To capitalize on these trends, MENA businesses should leverage advanced technologies, analytical dashboards, and sophisticated payment analytics for fraud prevention, personalization, and data-driven decision-making. Embracing innovation and adaptability will be key to leading the region’s digital payments revolution.